For many small business owners, the end of the year brings a familiar sense of stress. It’s the time you start trying to piece together your financials to understand what your profit and loss statement looks like and, more importantly, what your tax liability will be. It’s a scramble to make sense of the numbers and figure out what the next year’s tax bill will look like.

This often leads to a reactive posture. You discover your full financial picture in February of the following year, long after the window has closed to make strategic moves that could have saved you thousands. It can feel like you’re simply bracing for impact, with no ability to change the outcome.

But what if you could shift from being reactive to proactive? A recent Q&A session with business owner Richard Marvel and accountants Ryan and Karen from FirmTrack Solutions revealed a few powerful insights that can change this dynamic. As a financial strategist, I see this reactive scramble all the time, and their conversation perfectly highlighted three shifts in thinking that can break the cycle.

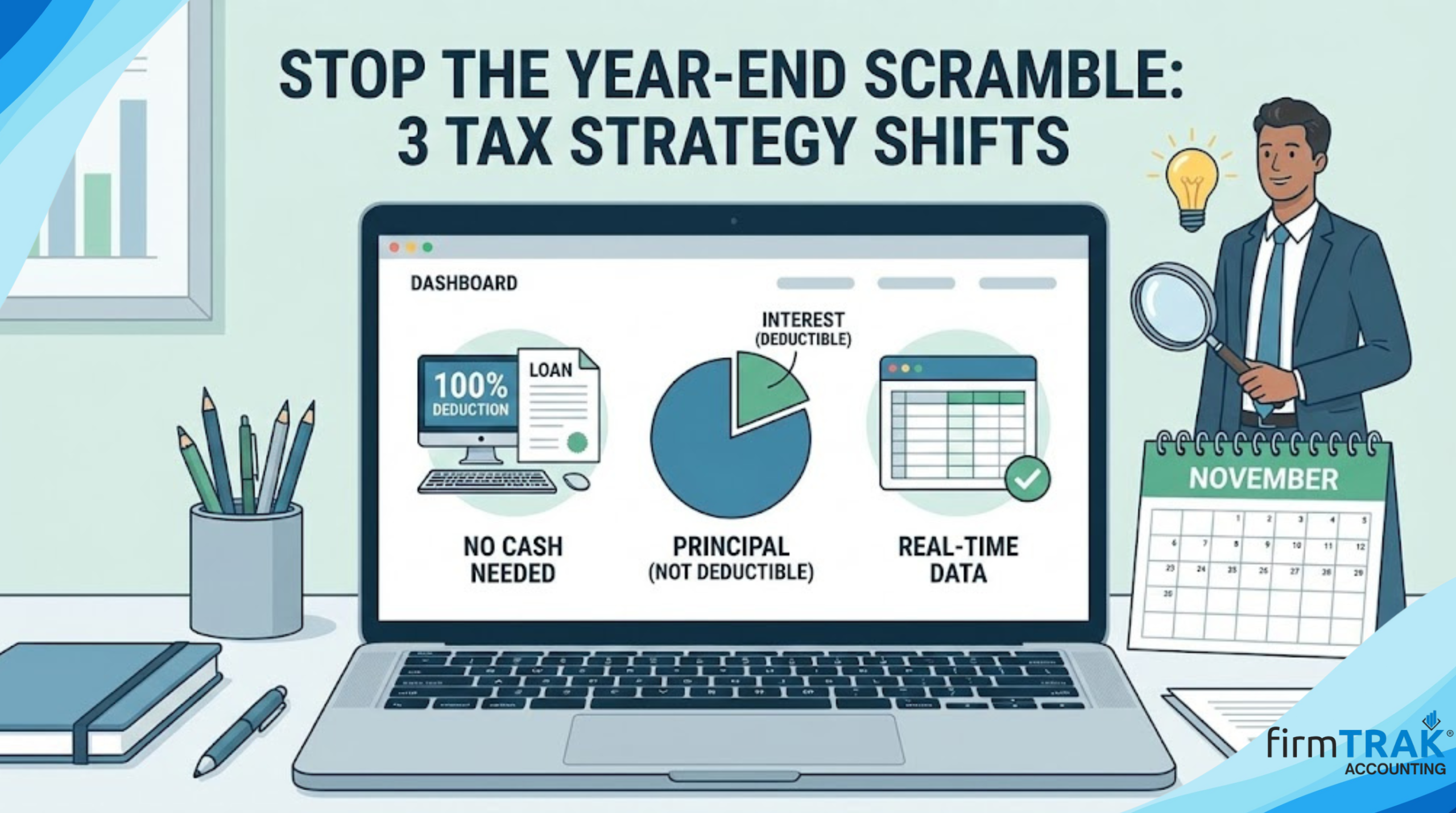

Takeaway 1: Myth: You Need Cash to Claim a Write-Off. Reality: You Only Need to Acquire the Asset.

Let’s tackle the biggest mental hurdle I see business owners face. The central question Richard posed to his accountants was a common one: how can I get a big tax write-off to offset income if I don’t have the cash on hand to make a big purchase? Many owners believe if they don’t have $25,000 in their operating account, they can’t possibly get a $25,000 tax write-off. This isn’t true.

Thanks to tools like bonus depreciation, you can get a 100% deduction for certain assets in the year you acquire them. For example, if you need $25,000 worth of new computers to offset your income for 2025 but don’t have the cash, you can finance the purchase. Even though you haven’t paid for the computers outright, you can still take the full $25,000 deduction in 2025.

The core insight here is that the act of acquiring the asset (the purchase) and the act of paying for it (the financing) are two separate transactions in the eyes of tax law. Transaction one is the purchase: you add a $25,000 asset (computers) to your books. Transaction two is the financing: you add a corresponding $25,000 liability (the loan) to your books. The tax deduction is tied to the acquisition of the asset, not the cash leaving your bank.

As accountant Ryan explained:

You’re basically creating two separate transactions on your books and they they go from there based on the tax rules…

Takeaway 2: Myth: Your Entire Loan Payment is a Deduction. Reality: Only the Interest Counts.

This naturally leads to the next question, which the business owner in the discussion immediately asked: what happens in the following years with the loan payments? Like many owners, his initial thought was that the entire payment must be a write-off. The accountants were quick to clarify this critical, and often misunderstood, distinction.

It’s critical to understand that your loan payment consists of two distinct parts:

• Principal: This is the portion of the payment that reduces your loan liability. Since you already received the full tax benefit upfront via bonus depreciation, paying down the principal is not a deductible expense.

• Interest: This is the cost of borrowing the money. The interest portion of your loan payment is a deductible expense that reduces your taxable income over the life of the loan.

If your loan has a 2.5% interest rate, only the small portion of your monthly payment covering that interest is deductible—the rest is simply paying down the principal you already got a deduction for. This is more than just a bookkeeping rule; it’s essential for cash flow forecasting. If you mistakenly think your entire loan payment is lowering your tax bill, you will be in for a nasty surprise.

Takeaway 3: Your Most Powerful Tool is Proactive Bookkeeping

This brought Richard to his personal “aha” moment: while tax tactics like bonus depreciation are powerful, they are only effective if you have the information needed to use them. The ultimate financial strategy isn’t a secret loophole; it’s having real-time, accurate information about your business’s performance.

Consider these two scenarios Richard described:

• The Old Way: Waiting until February of the next year to reconcile all income and expenses from the previous year. By then, it’s too late to make any tax-saving moves.

• The New Way: Having up-to-date monthly reporting that provides a clear picture of your profit and potential tax liability before the year ends.

This timely insight is what transforms you from a passive observer to an active strategist. When you know where you stand financially in November, you can make an informed decision to purchase that new equipment and take advantage of bonus depreciation. Without that data, you’re flying blind.

Richard perfectly described the feeling of being powerless without current data:

…it’s almost like I’m watching a crash happen in front of me and there’s not a thing I can do about it because I don’t know what my financial picture is for 2025 until the next February…

Conclusion: From Reactive Panic to Proactive Planning

The key to reducing your tax liability and making smarter business decisions is shifting from a reactive, year-end panic to proactive, year-round planning. By understanding that acquiring an asset (Takeaway 1) is separate from paying for it, and that only the interest on that payment is deductible later (Takeaway 2), you can see why real-time bookkeeping (Takeaway 3) is the linchpin that makes these powerful year-end decisions possible.

Understanding that you can finance a major purchase and still claim an immediate, significant tax deduction is the first step. Pairing that knowledge with timely financial reporting empowers you to take decisive action that can fundamentally change your company’s financial outcome for the year.

Now that you know what’s possible, what one decision could you make before year-end to change your financial future?