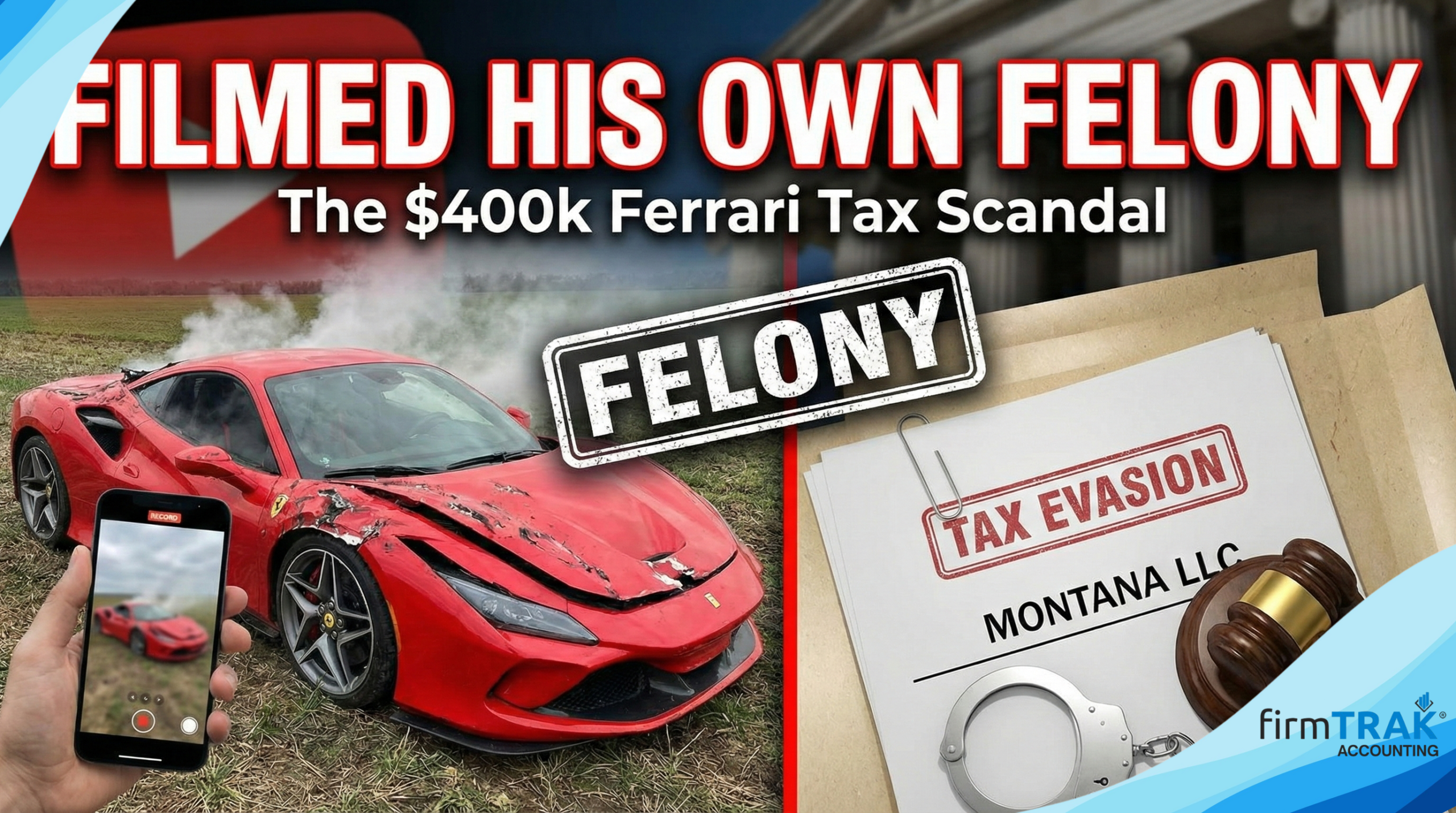

The economy of internet spectacle has produced many strange business models, but few are as viscerally destructive as that of WhistlinDiesel. Known to millions as Cody Detweiler, he built a massive following by destroying incredibly expensive vehicles for views—a profession built on shock, awe, and the crunch of high-end machinery. But the latest shock wasn’t a stunt. It was the news of his arrest for felony tax evasion, an investigation centered on a $400,000 Ferrari F8 he had famously documented himself destroying.

Beyond the sensational headlines of a YouTuber’s clash with the law, this case reveals surprising and critical lessons about tax law, the permanence of digital evidence, and a quiet but intense conflict happening between U.S. states.

The “Montana Loophole” Isn’t a Get-Out-of-Jail-Free Card.

The scheme, often touted in wealthy circles as a clever “hack,” involves registering a limited liability company (LLC) in Montana to purchase a high-value vehicle. Because Montana has no statewide sales tax, the buyer hopes to avoid paying taxes in their home state. The problem is that tax authorities are clear: this is not a loophole, but a direct violation of use tax laws. While Montana has no sales tax, a home state like Tennessee enforces a use tax on items purchased elsewhere but used primarily within its borders. Failing to pay it is a crime.

In Detweiler’s case, the financial stakes were high: a 400,000 Ferrari F8** and an estimated **28,000 in evaded use tax. Such a brazen scheme suggests he may not have acted alone. As Ryan of firmTRAK Solutions speculates, “he’s probably got an advisor who knew about it and told him to do it.” Given the public nature of his activities, financial professional Carin Weiss-Krolikowski finds it difficult to believe this was an accident:

He had to have known that if you buy something out of state and you live in a different state, you’ve got to pay the use tax. It doesn’t matter where you buy it.

The Ultimate Irony: His Content Became the Evidence.

The central irony of Detweiler’s situation is that his entire profession—publicly documenting his activities—created an irrefutable evidence trail for prosecutors. The public record he meticulously created was damning, undermining any claim that the vehicle was based in Montana. His own content established the key facts of the prosecution’s case:

- He lives and operates primarily in Tennessee, establishing a clear tax nexus that makes him liable for the state’s use tax.

- The Ferrari, supposedly owned by a Montana LLC, was filmed being destroyed in Waco, Texas, proving it was not being used in Montana.

This self-documentation is a prime example of what Weiss-Krolikowski described as handing ammunition to investigators. “You’re handing evidence over to the prosecution and the law to prosecute you,” she explained. The most practical takeaway from this saga is a simple and powerful piece of advice offered by Ryan from firmTRAK Solutions: “don’t film your felonies.”

One Influencer’s Stunt Exposed a Quiet War Between States.

While the YouTuber’s actions may seem “really dumb on its face,” they inadvertently cast a spotlight on a complex and ongoing “contest that’s happening between the states” regarding tax policy. This isn’t just a story about one individual’s alleged crime; it’s a window into conflicting state interests. Montana benefits from the revenue generated by LLC registration fees and, more fundamentally, is “kind of constitutionally against these types of taxes,” giving it little incentive to curb the practice.

This philosophy puts it at “cross purposes” with states like Tennessee, which are fighting to collect legitimate use tax revenue they are owed. A high-profile case like this brings a typically overlooked issue of interstate tax competition into public view, highlighting the lengths to which states will go to protect their tax base from being eroded by those exploiting differences in state law.

Conclusion: A Modern Cautionary Tale

The WhistlinDiesel scandal serves as a uniquely modern cautionary tale with three clear lessons: a popular tax “hack” is a serious felony, public content is also public evidence, and the seemingly isolated actions of an individual can illuminate far larger systemic conflicts.

This case forces us to consider the blurred lines in our hyper-documented world. In an economy driven by monetized transparency, how does one calculate the ROI on a stunt that generates millions of views but culminates in a felony indictment?